The Evolution of Cyber Insurance: From Legal Afterthought to Business Essential

May 11, 2026

If you walked into an insurance office 25 years ago and asked for a "cyber policy," you would have likely received a confused look and a stack of generic paperwork. Today, cyber liability insurance is one of the most critical components of any risk management strategy. And the requirements to obtain it have never been stricter.

Understanding how this industry evolved helps explain why insurers now scrutinize your technical controls before issuing a quote, and why businesses that haven't kept pace are finding coverage harder to get.

Download the STACK Cybersecurity Cyber Liability Insurance Checklist

The Early Days: Errors and Omissions

In the late 1990s, the internet was still a frontier. Most businesses used it for basic email and static websites. What we now call cyber insurance was tucked inside Errors and Omissions (E&O) policies, originally designed for software developers and tech providers. If a programmer made a mistake that crashed a client's server, the policy covered the financial fallout. Coverage was about human error, not criminal intent. The idea of a global criminal network locking your files for a digital ransom felt like science fiction.

The Turning Point: Privacy Law Changes Everything

The mid-2000s changed the equation. As businesses began storing massive amounts of customer data such as credit card numbers, Social Security digits, and medical records, the stakes rose dramatically. California passed the first data breach notification law in 2002. It went into effect on July 1, 2003.

Suddenly, losing customer data meant legal obligations that included notifying affected individuals, retaining counsel to navigate state statutes, covering mailing costs for thousands of letters, and funding credit monitoring services for those impacted.

Insurers recognized that existing E&O policies weren't built for this. The result was the birth of the standalone cyber liability policy, initially focused on what the industry called "Privacy Liability" coverage.

The 2010s: Ransomware Changes the Market

By the 2010s, cybercriminals had discovered something more efficient than stealing data: locking it. Ransomware began hitting businesses of every size. High-profile attacks like WannaCry and NotPetya demonstrated a single piece of malware could cause billions of dollars in global damage within hours.

For several years, cyber coverage was relatively easy to obtain. Policies were inexpensive, and insurers often paid ransoms quickly to restore operations. But that approach created a cycle that emboldened hackers and drove up claims. Premiums climbed. Underwriting standards tightened. The industry entered what analysts called a "hard market," and it has not fully relaxed since.

Note STACK Cybersecurity and most security professionals strongly recommend against paying ransoms. They often aren't effective at getting data released. The funds paid support global criminal enterprises. And paying a ransom nearly guarantees you'll get hacked again. Read more about why we think the U.S. and all nations should ban ransomware payments.

Where We Are Today: The Safety Inspection Reality

The insurance industry is no longer a passive observer. Insurers now act more like digital health inspectors, reviewing your technical controls before agreeing to cover you. Because ransomware payouts became so costly, carriers can't afford to insure businesses with poor security hygiene.

Applying for a policy today means answering detailed technical questions. Multi-factor authentication is no longer optional: if MFA isn't protecting your email and remote access systems, many insurers will deny coverage outright. Endpoint detection and response tools are expected to be in place so threats can be identified and contained before spreading. Immutable backups are required to prove that your recovery data can't be wiped alongside your live systems in an attack.

These aren't arbitrary checklists. Each requirement reflects a hard lesson learned from a real category of loss. Businesses that meet them are statistically less likely to file a claim — and insurers price accordingly.

Why Stricter Requirements Are Good for Business

The tighter underwriting standards can feel like another compliance hurdle. But the controls insurers require are the same ones that meaningfully reduce breach risk. MFA alone blocks the vast majority of credential-based attacks. Regular, tested backups are the difference between recovering from ransomware in hours and paying a six-figure ransom with no guarantee of getting your data back.

"The requirements insurers have put in place aren't just about managing their risk. They're a roadmap for building a security posture that actually holds up," said Rich Miller, founder and CEO of STACK Cybersecurity. "If you treat the underwriting questionnaire as a security checklist, you'll end up better protected and more insurable at the same time."

The companies that struggle to obtain coverage today often find they have deeper security gaps than they realized. The application process itself can be a useful diagnostic, surfacing vulnerabilities that would otherwise go unaddressed until a breach forces the issue.

Making Sure Your Coverage Keeps Pace

Cyber insurance requirements continue to evolve as the threat landscape shifts. A policy that was sufficient three years ago may no longer reflect current underwriting standards — or current risk exposure. Businesses that haven't reviewed their coverage recently may be underinsured, paying for a policy with exclusions that would apply precisely when they need coverage most.

The question isn't only whether you have a policy. It's whether your technical controls meet today's requirements, whether your coverage limits reflect your actual exposure, and whether your insurer understands your industry's specific risk profile.

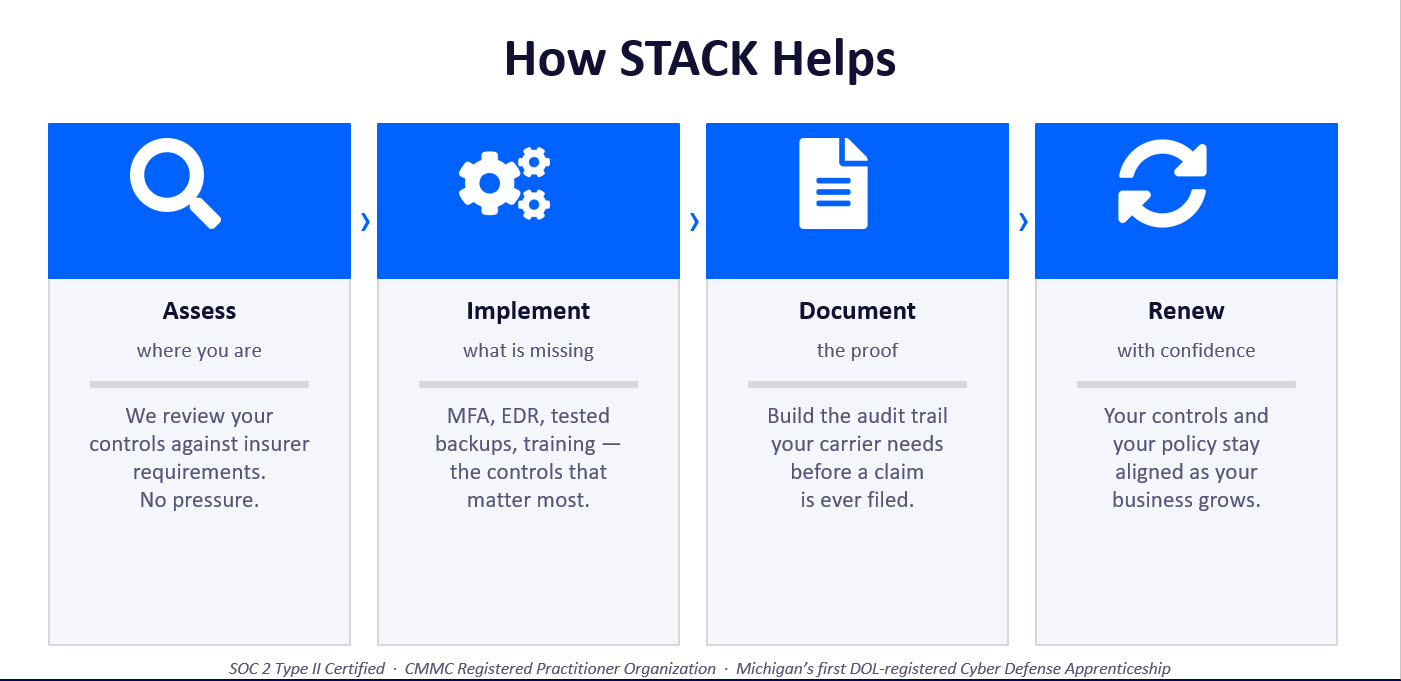

STACK Gets You Insurable

As a trusted IT service provider, we'll support your business beyond basic IT and help you build a foundation that cyber insurers trust and reward. We'll start by assessing your environment and identifying what's missing, from MFA and antivirus to policy documentation and employee training. Then, we'll tailor solutions that align with both your business goals and insurer expectations. We'll also go beyond implementation and make sure everything is documented and audit-ready, because paperwork is just as important as protection.

Email: info@stackcyber.com

Phone: (734) 744-5300

Contact Form